This is about the thing nobody sat a lot of us down and told us - the ones who work for a living - and the sixty seconds it takes to find out if it reaches you too.

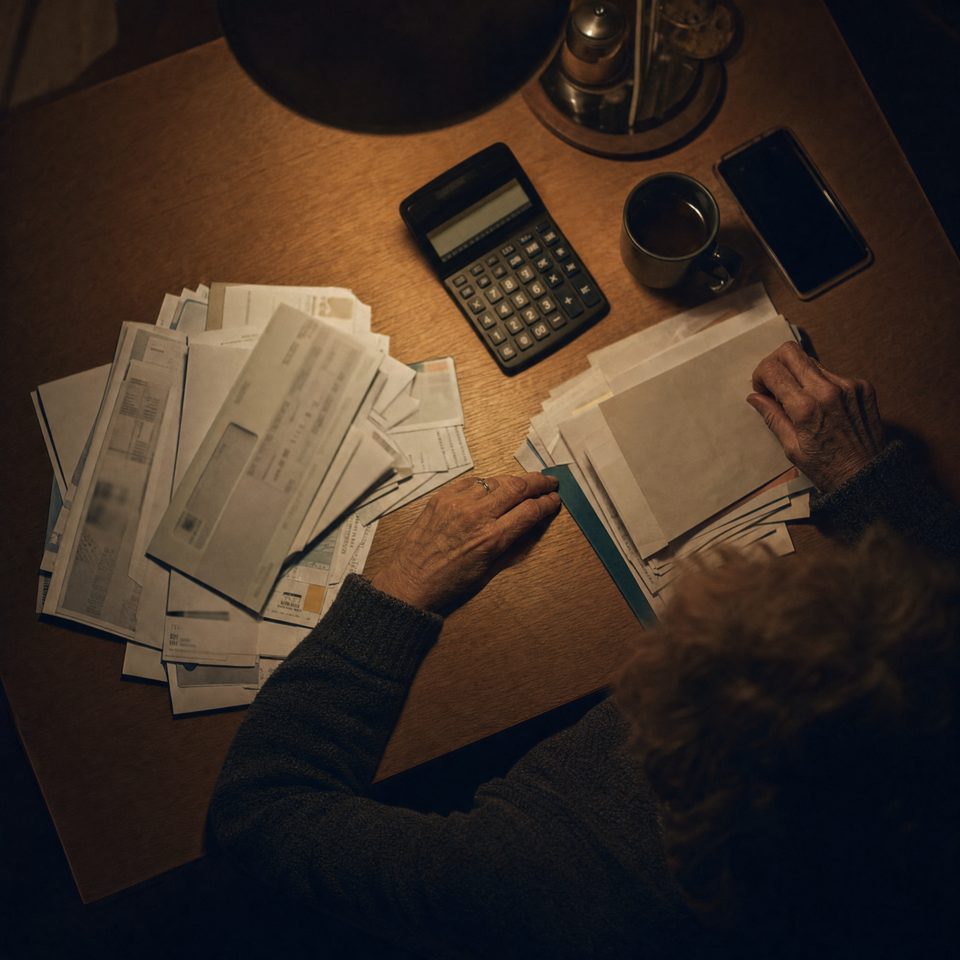

You know the arithmetic without ever writing it down. Gas. The light bill. The phone. The little bit you send your daughter when her car acts up again. There's a number at the bottom of all that, and there has never once been room in it for a doctor.

So you got good at going without. You keep the Advil in three places so you're never caught without it. You split the one prescription you can't skip with a butter knife on the kitchen counter, because half a pill is still a pill and the bottle lasts twice as long that way. Maybe there's something you've been meaning to get looked at - a lump, a tooth, a cough that won't quit - the kind of thing you noticed back in the spring, and it's summer now, and you keep telling yourself you'll deal with it when you have to. A lot of people know that exact feeling.

It's not about being old. It's the kind of tired that sleeping doesn't fix - the kind a lot of people who work on their feet all day know by heart. And it's not about being bad with money either. If anything, you're the best with money you know. You get sixty kids home safe every single morning, or you stock the shelves before the store opens, or you turn the patient so she doesn't get sores, and then you drive home and you don't get your own self looked at, because looking costs money you've already spent in your head three times over.

You looked once. Maybe twice. Years ago somebody said the words health insurance and you saw a number with a comma in it and closed the laptop, because a number like that isn't a real option, it's a joke somebody's playing on you. You figured those plans were for people with desk jobs and dental printed on the pay stub. Not for people like you.

So you made your peace with it. You told yourself you're healthy enough. You told yourself you'll deal with it when you have to. You made the appointment for the tooth you've been chewing around since spring, and then you canceled it, because the light bill came the same week and the light bill always wins.

And underneath all of it sits the real fear, the one you never say out loud. It isn't the dying. It's the bill that comes before the dying. It's the thought of working your whole life and still ending up a burden to your own kids.

"It's not the dying I'm scared of. It's the bill that comes before the dying."

Here is the thing nobody ever sat you down and told you.

There is a place called the Marketplace. And for a lot of people under 65 who work for a living and earn a modest income, there's help built right into it - a premium tax credit. It is not a check that lands in your mailbox. It is not cash you can hold. It goes straight to the insurance company every month, and it knocks the price of a real health plan down. For a lot of people on a modest income it brings the monthly cost down to a fraction of what they'd ever guess. For some, close to nothing at all.

Not a discount card. Not a coupon in the mail. A real health plan. Doctor visits. Prescriptions. Dental and vision. The kind of plan you always assumed was only for the people who had it printed on their pay stub.

The only catch is that nobody knocks on your door to tell you. You have to check. And the checking turns out to be almost stupidly small - about sixty seconds and three questions. People started calling it the 60-Second Coverage Check, because honestly that's all it is: a way to find out, in under a minute, whether the help reaches you.

Now, I know exactly what that does to a certain kind of person. The proud kind. The kind who has never asked anybody for a single thing in her life and isn't about to start now.

So let's be plain about what this is and what it isn't.

It is not charity. It is not a handout. It is not free money, and it is not cash you can spend at the store. It's a real health plan, and the Marketplace helps pay the premium - the very same way a lot of jobs help pay it for the people lucky enough to have that kind of job. You just never had the kind of job that did it for you. That is the only difference between you and them.

This help has been sitting there the whole time. It was built for exactly the person who works hard, earns a modest living, and got skipped. The only thing you ever did wrong was not know it was yours to claim. You don't want charity. You want what's fair. This is the what's-fair kind.

Elizabeth

Let me tell you about Elizabeth.

She's 60. She drives a school bus in Seguin, Texas. Single. Makes about thirty-five thousand a year and hadn't carried insurance in years. She had every reason you have to be certain this wasn't for her, and she said all of them out loud before she'd even try.

"I keep Advil in the glovebox, the console, and my purse," she told the agent. "That's my health plan. Sixty kids get home safe every single day because of me, and I can't afford to get my own self looked at."

For a driver it's worse than for most, because the medical card is the job. The physical stands between her and the license, and the license stands between her and the light bill. So she couldn't afford to be found sick. She stayed away from the doctor precisely because she couldn't afford whatever he might find.

Then she ran the check. It took less than the length of one red light. A licensed agent got on the phone with her and walked her through what she actually qualified for. One call. Eight minutes and change.

Here is what it came to, in her own words: "Zero dollars a month for the plan. Ten dollars to see the doctor. Five dollars for my prescription. I sat in my driveway and I cried, and I am not a woman who cries."

She said yes before the agent even finished laying out her options. Eleven years of telling herself the door was shut, and she was ready the second it cracked open.

That check Elizabeth ran? You can run the exact same one, right now, from wherever you're sitting. It's free. It's about sixty seconds. Three questions. If you'd rather read the rest of how this works first, go ahead - it'll still be here when you're done. But if you already feel it, you don't have to wait for permission to find out.

Elizabeth isn't rare. That's the part that should make you angry and hopeful at the same time.

A lot of people under 65 are finding the exact same thing right now. Drivers. Warehouse workers. Home health aides. Cooks, cashiers, cleaners, the people who turn the patients and stock the shelves and get the kids home safe. People who spent years dead certain the help was meant for somebody else, running a sixty-second check and finding out it was theirs the whole time.

Eligibility varies. It comes down to your age, your income, your household - which is exactly why the check exists, and exactly why a licensed agent confirms it instead of some promise printed on a page. Nobody can tell you what you qualify for until you actually look. But a lot of people who were every bit as sure as you are looked anyway, and turned out to be wrong in the best possible way.

There are also set windows during the year when you can enroll, and certain changes in your life can open one just for you. A licensed agent can tell you whether a window's open for you right now. It's one more reason not to hand this to a someday that keeps not arriving.

Somewhere in your car right now there is a bottle of Advil. Glovebox, console, or purse. You know exactly where it is.

You can leave it there. You can keep splitting the pill with the butter knife, keep meaning to get the tooth looked at, keep doing the math that never has room in it. That's one road. It's the road you're already on, and it costs you nothing today and everything slowly.

Or you can take sixty seconds - less time than one red light - and simply find out. Not commit to anything. Not spend a dime. Just find out whether the door that opened for Elizabeth opens for you too.

You have carried everybody else for years. Sixty kids. A daughter. A mother. Patients who don't remember your name by morning. This is the one thing that asks you to do something for the person who has been quietly doing everything: find out what is already yours.

Take the sixty seconds

The check is free. It takes about a minute. Three questions - your age, your income, your household - and it tells you whether it looks like you may qualify. If it does, a licensed agent picks up and walks you through your real options on the very same call. No cost. No obligation. No pressure. A real person on the line, not a form and not a robot.

If it turns out you don't qualify, you've lost sixty seconds and now you know for sure, which beats another eleven years of just assuming. And if you do qualify, you might be the one sitting in your own driveway soon, finally doing the thing you never do for yourself.